SBA 7(a) vs. SBA 504 Loans: What Lenders Look For & Common Questions Answered

If you’re exploring SBA financing, two programs come up more than any others: SBA 7(a) and SBA 504 loans. While both are backed by the Small Business Administration, they serve very different purposes—and lenders evaluate them differently.

Here’s a practical breakdown of how each program works, what lenders focus on, and the most common questions borrowers should expect.

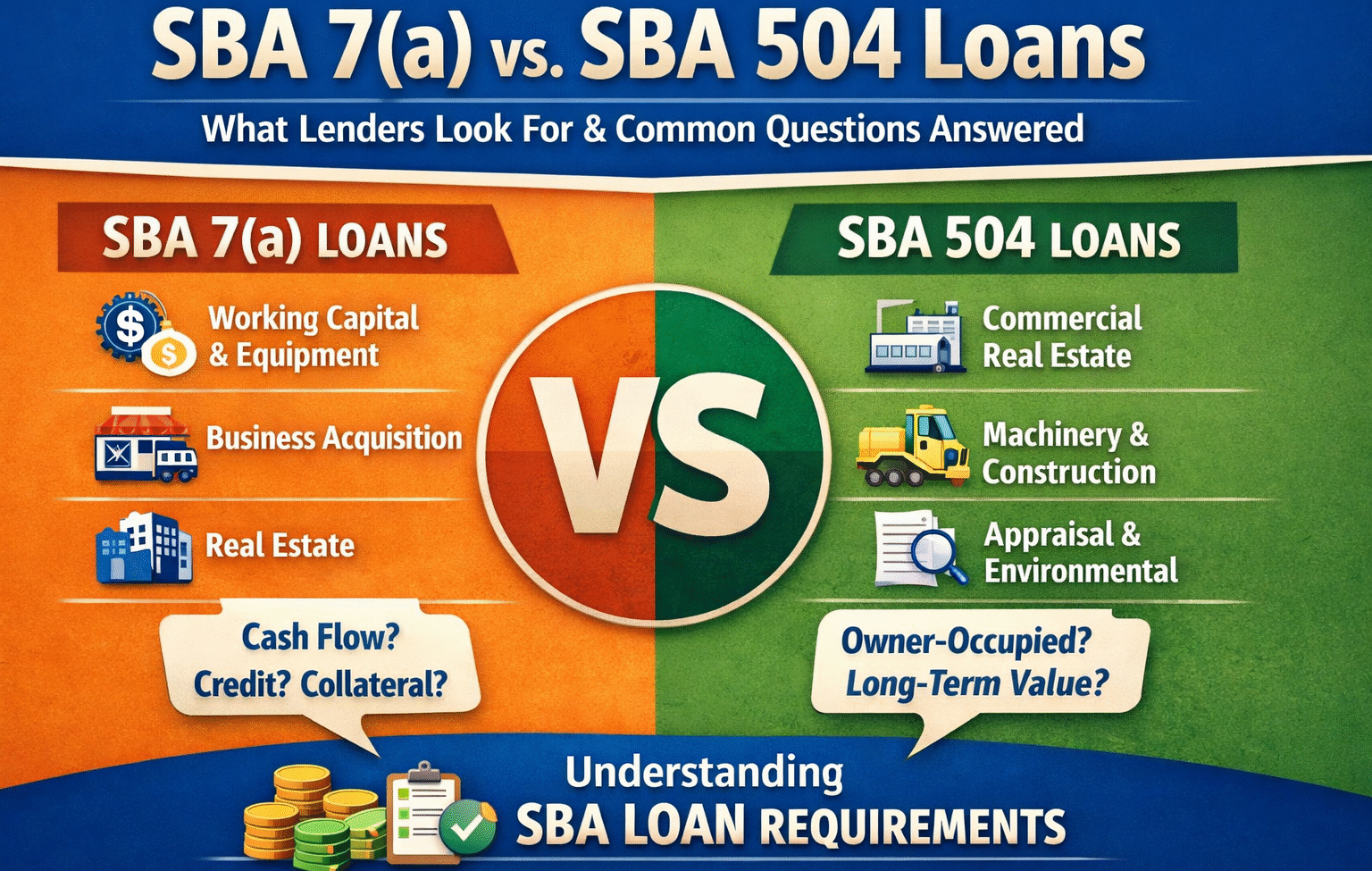

SBA 7(a) Loans: Flexible Financing for Growing Businesses

The SBA 7(a) loan program is the most flexible SBA option and is commonly used for:

- Working capital

- Business acquisitions

- Equipment and machinery

- Inventory

- Debt refinance

- Owner-occupied commercial real estate

Key SBA 7(a) Loan Basics

- Maximum loan amount: $5 million

- SBA guarantee: Up to 75–85% (depending on loan size)

- Loan terms:

- Working capital: up to 10 years

- Equipment: up to useful life

- Real estate: up to 25 years

- Interest rates: Typically variable or fixed, based on Prime

- Down payment: Often 10–20%

Because of its flexibility, the 7(a) program is popular—but that also means lenders look closely at cash flow and borrower experience.

Common SBA 7(a) Lender Questions

What is the loan being used for?

Lenders must confirm the use of funds is SBA-eligible and clearly defined.

How strong is cash flow?

Most lenders look for a Debt Service Coverage Ratio (DSCR) of at least 1.15x to 1.25x.

How long has the business been operating?

Startups can qualify, but they typically require stronger equity, experience, or collateral.

What is the borrower’s experience?

Industry experience helps mitigate risk and strengthens approvals.

What does personal credit look like?

A credit score of 680+ is generally preferred.

What collateral is available?

SBA loans do not require full collateral coverage, but lenders must take available assets.

SBA 504 Loans: Long-Term Fixed Asset Financing

The SBA 504 loan program is designed specifically for major fixed assets, making it ideal for:

- Owner-occupied commercial real estate

- Heavy machinery and equipment

- Construction or significant renovations

🚫 SBA 504 loans cannot be used for working capital or inventory.

How the SBA 504 Structure Works

- 50% – Bank or lender (first lien)

- 40% – SBA via a Certified Development Company (CDC)

- 10% – Borrower down payment

- 15–20% for startups or special-purpose properties

Key SBA 504 Loan Features

- Maximum SBA portion: $5–$5.5 million

- Interest rates: Long-term fixed (often very attractive)

- Loan terms:

- Real estate: 20–25 years

- Equipment: 10–20 years

This structure reduces risk for lenders while offering borrowers stability and lower equity requirements.

Common SBA 504 Lender Questions

Is the property owner-occupied?

The business must occupy at least 51% of an existing building.

Is the asset essential and long-life?

Equipment must have sufficient useful life and be integral to operations.

What is the appraised value?

The appraisal must support the full capital stack.

Are there environmental concerns?

Environmental reviews (often a Phase I ESA) are standard for real estate.

Is this a startup or special-use facility?

These factors increase risk and typically require higher down payments.

Questions Lenders Ask for Both SBA Programs

Regardless of the program, lenders almost always ask:

- Who are the guarantors? (20%+ owners must personally guarantee)

- What does global cash flow look like?

- Are financial projections realistic and supported?

- Are there tax issues, liens, or prior credit events?

- What is the borrower’s contingency plan if revenue declines?

Final Thoughts: Preparing for SBA Financing

Borrowers who understand how lenders think move through the SBA process faster and with fewer surprises. Clear financials, realistic projections, and properly valued assets go a long way toward approval.

Whether you’re financing a business purchase, real estate, or equipment, choosing the right SBA program—and preparing for lender questions upfront—can make all the difference.